“If you have a model where revenue risk is taken away from the operator, and instead you incentivise punctuality, performance and delivery for passengers, it creates a different dynamic. That’s what we have done on London Overground, and it is equally deliverable in the other great urban centres.

“Manchester is the most well-developed parallel - it is key that there is well-developed political leadership. That doesn’t necessarily mean a Mayor, as we have. But there must be a single coherent voice that represents the urban area overall, coalescing disparate views.”

The West Midlands

West Midlands Rail will follow Rail North’s lead. In March, the Secretary of State formally agreed the process that will lead to rail devolution.

“While there are many similarities, West Midlands Rail will have governance structures more suited to local conditions,” says Toby Rackliff, rail strategy manager for the West Midlands Integrated Transport Authority. We will be looking jointly to specify and manage local rail services in the West Midlands travel-to-work area, in partnership with the DfT.”

West Midlands Rail is a group of seven metropolitan authorities and seven shire and unitary local transport authorities. Above it will sit Midlands Connect, similar in scope to Transport for the North.

WMR’s target is to create a more efficient railway that offers better value for the taxpayer, drives growth and reduces subsidy. Its proposition states: “Having a targeted, locally accountable contract with proper incentives on the operator will enable WMR to specify and manage rail services more effectively than the current national arrangements.”

The organisation aims for a single identity for the local rail network, a consistent fare structure across routes and operators, a common smartcard, and a standard approach to information. It would operate 112 stations and run more than 650 services a day, carrying 30 million passengers a year.

“The new London Midland franchise will commence in June 2017,” explains Rackliff. “It is likely to run until 2024, but will in any case need to expire before the opening of HS2 in 2026, as this will require a re-mapping of services on the West Coast Main Line.

“The DfT wishes to keep the current London Midland franchise geographic area, which will (for example) enable through London-Birmingham semi-fast services via Northampton to be retained. However, it is proposed that there will be a separate WMR business unit with its own distinct identity within the new franchise, and this will be the focus of the devolution proposition.”

It is proposed that the initial contract follows DfT standard arrangements, with the operator taking revenue risk. But during the franchise WMR would progressively take on greater management responsibility, and be in a position to take the revenue risk itself in subsequent contracts.

“There is a non-devolution model which still gets results,” points out CBT’s Joseph. “Groupings of local authorities such as the East Midlands Rail Forum can help to bring forward modest upgrades, such as easing of speed restrictions to make small journey time improvements.

“You don’t need devolved control to make progress, but you

do need strong local authority partnerships. That said, Jonathan Denby at Abellio Greater Anglia and its predecessors has almost single-handedly co-ordinated a rail strategy for his region, and brought every local authority onto his side. A first result is the ‘Norwich in 90’ policy.

“There are opportunities for regions which don’t want to go the whole hog. In the South West, they don’t really want to split away from the rest of the country. That’s because they do rather well out of the cross-subsidy that flows from a single operation running long-distance inter-city and local branch lines. They think separating them in a Rail North style would be counter-productive.

“But the principle of local control is without doubt. When snow is disrupting Merseyrail, the people in Merseytravel can see it is snowing, as they have to get home on the trains, too. So they can work with the train operators to ease the impact and manage the paperwork afterwards. The Department for Transport only sees the drop in performance data without understanding what caused it.”

Regional economic growth

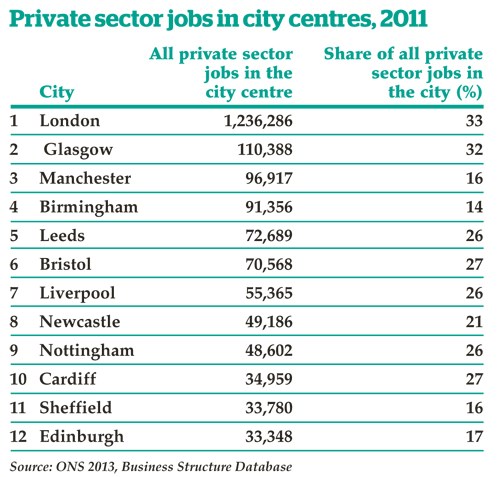

London and the South East drive the UK’s economy. Recent figures show that the UK economy grew by 0.8% in the first quarter of 2015… but the economy is not growing evenly.

The Centre for Cities has produced a report (Fast Track to Growth, 2014) arguing that the economic divide between north and south is growing. The paper found that growth had been mainly driven by cities in southern England - for every 12 net new jobs created between 2004 and 2013 in cities in the south of England, only one was created in cities throughout the rest of Great Britain.

The independent research organisation said the number of jobs created in London rose by more than 17% between 2004 and 2013. But in Blackpool, Rochdale and Gloucester, there were falls of 10%.

Centre for Cities called on all parties to oversee “significant devolution of both fiscal and structural power, providing incentives for cities to support economic growth, and giving greater flexibility to ensure money can be spent where it is most needed”.

This appears to match the emerging agenda of the new Government. In his final Budget of the previous Parliament, Chancellor George Osborne made a series of policy announcements relating to what is now termed the ‘Northern Powerhouse’.

“Working with Transport for the North, the Government will look at rolling out better roads, quicker journeys, and improved rail connections between the major cities of the North,” he said.

Centre for Cities researcher Dr Ilona Serwicka says: “The focus on city-region transport is important. Almost half of commuters in cities live and work in different local authorities, and this number is likely to increase. The census shows that in the past decade, the distance that commuters travel to work has increased. But many city-region transport networks remain fragmented.

“Successful cities need continued investment in transport to continue to be attractive places for businesses and people. They also need more control over how their transport systems operate, in order to deliver the more integrated and co-ordinated transport networks that people and firms depend on.”

London Overground

London Overground has been in existence for less than a decade, but already it has reshaped the capital’s rail map. And since May 31 it has grown even larger, with Abellio Greater Anglia’s inner suburban services transferring to Transport for London’s jurisdiction.

The routes are from Liverpool Street to Chingford, Enfield Town and Cheshunt via Seven Sisters, plus the separate Romford to Upminster line. These will now be operated by LOROL, the joint venture between Hong Kong’s MTR and Deutsche Bahn. MTR solo has taken on Liverpool Street to Shenfield as the first stage of its Crossrail concession.

Unlike most other train operating companies, London Overground is franchised by TfL and not by the Department for Transport. Prior to the latest absorption it already operated six lines and 83 stations. It carried 136 million passengers in the year to March 2014, and the inner West Anglia services will add another 20 million.

TfL says that as a result of regional control, new trains will be on the way. But the biggest change that passengers notice is lower fares. TfL says 80% of journeys cost less than before, and that no passenger will have to pay more because of the changes.

TfL says that as a result of regional control, new trains will be on the way. But the biggest change that passengers notice is lower fares. TfL says 80% of journeys cost less than before, and that no passenger will have to pay more because of the changes.

TfL sets fare levels, procures rolling stock, and determines service levels. The revenue split between TfL and LOROL is 90:10, and the franchise is due for renewal from November 2016.

“Our franchising model - a management concession - gives a better deal for passengers,” says TfL’s Mike Brown. “It focuses on a reliable railway, rather being there to generate income growth for the train operating company.”

Brown confidently predicts rapid growth under TfL’s stewardship. He points to a 268% increase in passengers on the North London Line since 2007, fuelled partly by the increasing size of London’s population.

He adds that work has started with a deep clean of all the additional stations, with redecoration, cameras and better customer information. “It’s not like we’re taking something that is in perfect working order,” he says.

TfL wishes to extend its direct influence further. It would like to acquire Southeastern’s metro services from Victoria, Cannon Street and Charing Cross, although Kent County Council has objected. So would those areas on the periphery of big devolved metropolitan railways lose out?

“I argued the case strongly when I made the bid to run the inner suburban parts of Southeastern last year,” says Brown.

“We ran into a lot of political opposition. Not party political, but geographical political from those outside the London boundaries who felt that their mid-distance services could somehow be diminished by a focus within London. My argument is that if you incentivise performance and reliability, then even at the margins you must get a benefit. Even for those routes outside the political governance area.

“We continue to make the case based on the evidence of what we are delivering. Our delivery record is the thing that will swing this. There will be a public cry for it. It is an inevitability. It is a matter of time. Southeastern - we want the routes out of London Bridge. Southern - the inner routes from London Bridge and Victoria. And South Western routes into Waterloo. You could almost draw a clockface around London. But the three big ones in the south are the ones I have my immediate eye on, because they are the ones where we can make the biggest difference - providing the south of London with the same level of metro service as those who live north of the river, and who get on the underground and the bits of overground that we already run.”